When was the last time you ordered a credit report? The paper document is abstruse enough, but you have to maneuver through the morass of oddly-named companies that produce them — Equifax, Experian, TransUnion and more.

When was the last time you ordered a credit report? The paper document is abstruse enough, but you have to maneuver through the morass of oddly-named companies that produce them — Equifax, Experian, TransUnion and more.

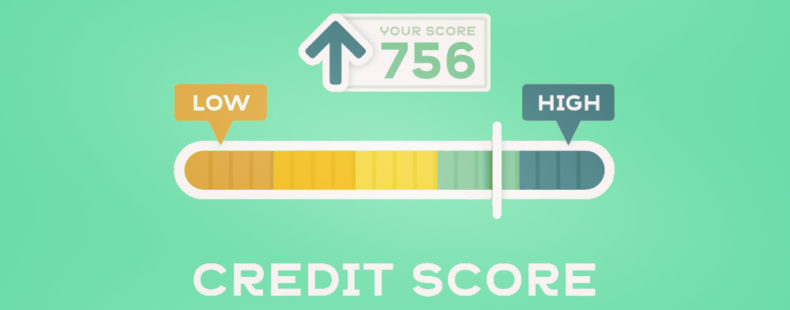

The process is abstract, but the results are concrete. There’s some new, and bad, news about those infamous numbers. More than a quarter of Americans now have scores of 599 or lower. Banks rarely approve loans for anyone below the 599 threshold.

Since our concern is words and not financial data, you won’t find here an elaboration of how the scores are generated or what different numbers mean for your wallet. Perhaps though, we can demystify a small but ubiquitous word in the cruel credit process. Why is it called a FICO score?

FICO is an abbreviation for the Fair Isaac Corporation, the first company to offer a credit-risk model with a score. The story would be more interesting if “Fair Isaac” refers to some wise, aboveboard person. Here’s the deal: Bill Fair and Earl Isaac are the founders. The combination of their surnames simply has a Biblical or Arthurian ring to it.

The credit score model devised by FICO in the 1950s is still a primary method for determining your creditworthiness. Unless you want a migraine, consider avoiding the details of the mathematics behind the scores. Take this test: one factor in the process can be a probit, which is “a normal equivalent deviate increased by five.” If the previous sentence feeds your curiousity, good thing you are on a dictionary Website. If the definition of probit makes you dizzy, take a breath and make sure you don’t confuse FICO with FICA (the Federal Insurance Contributions Act, how the government collects money for Social Security.)